Omninos Technologies

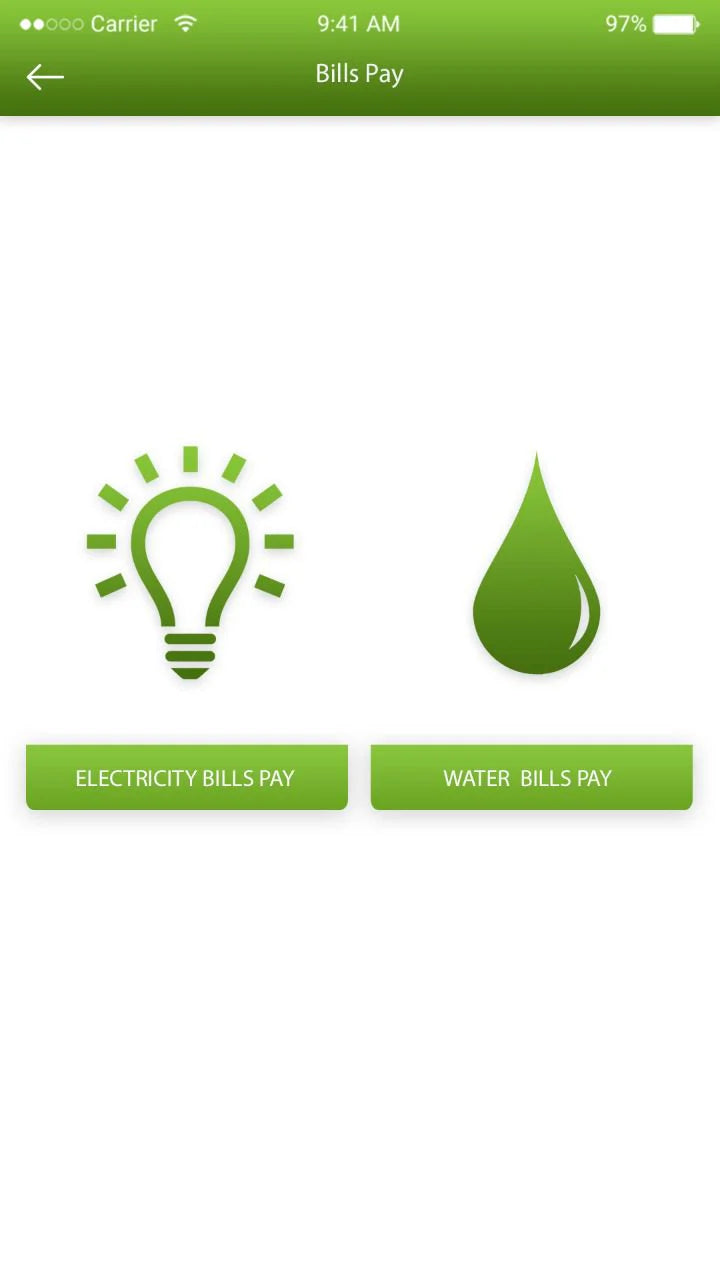

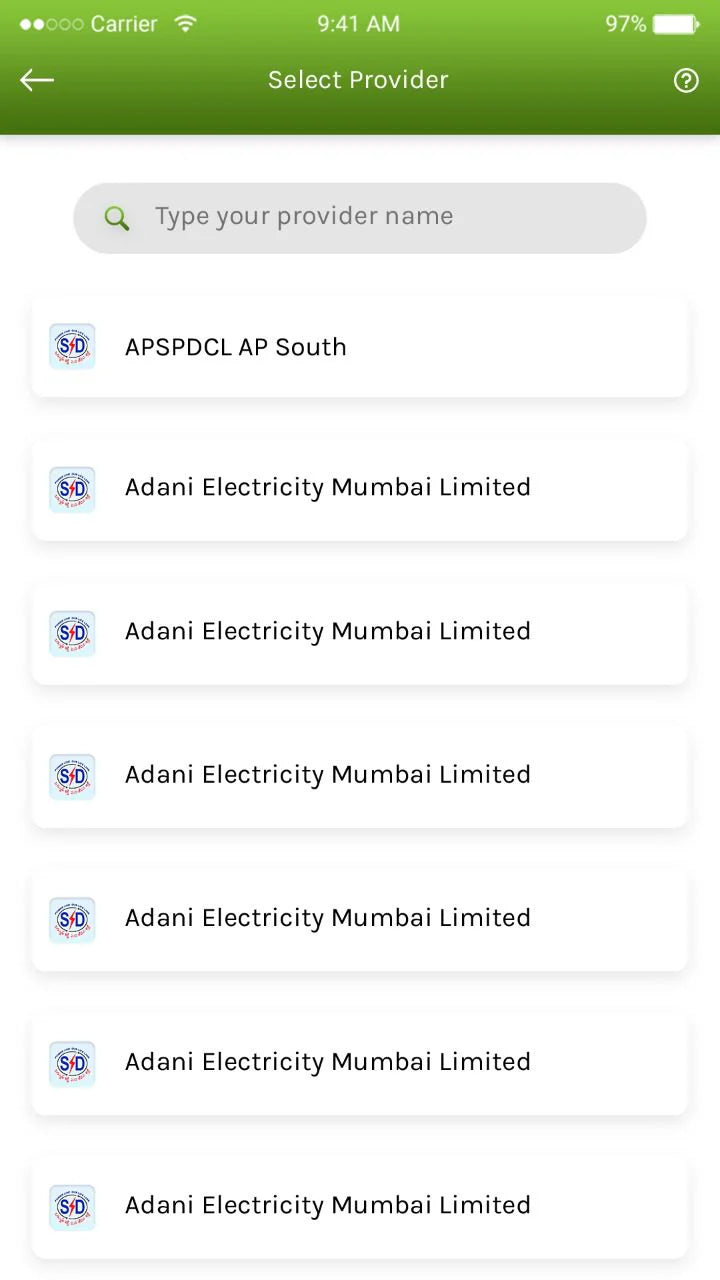

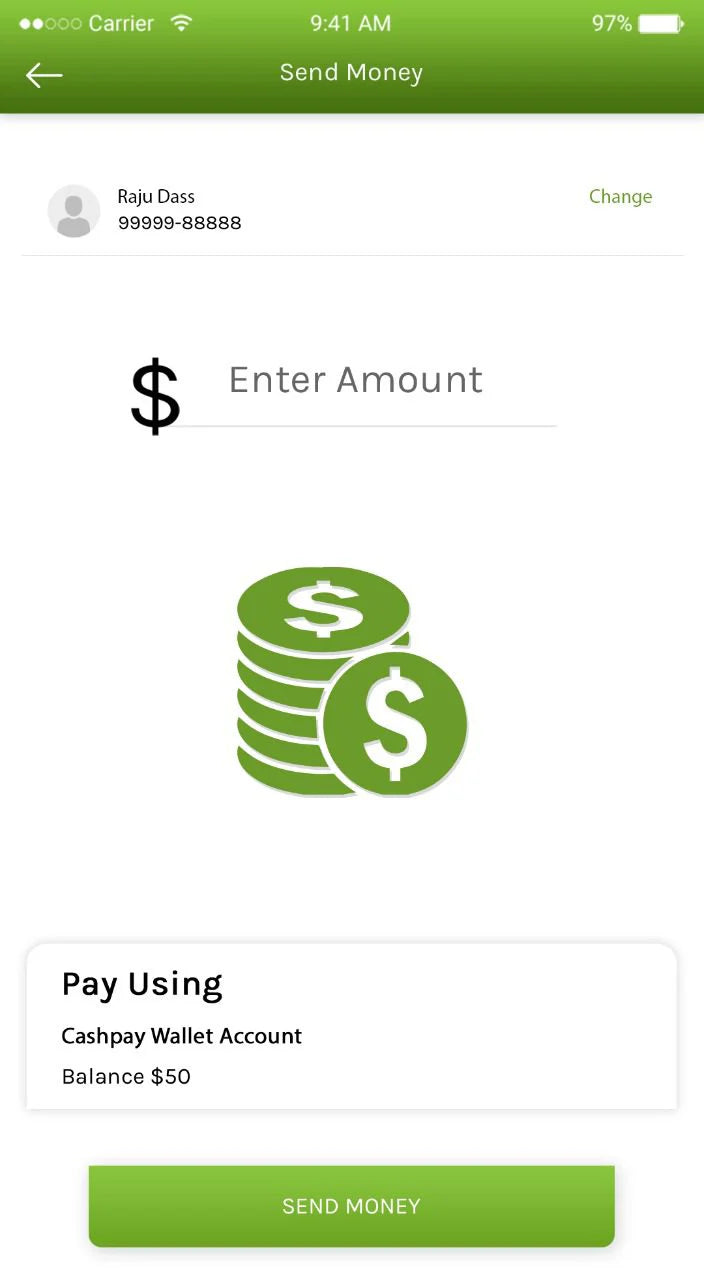

MyPCS: Mobile payment application

MyPCS: Mobile payment application

Couldn't load pickup availability

Introduction to Mobile Payments

Mobile Payments: A New Era of Financial Transactions

Mobile payments have revolutionized the way we handle financial transactions. In an increasingly digital world, the convenience and speed of mobile payments have made them an integral part of our daily lives. This introduction delves into the basics of mobile payments, exploring their benefits, how they work, and the future of this transformative technology.

What Are Mobile Payments?

Mobile payments refer to money transactions made through a mobile device, such as a smartphone or tablet. These transactions can include paying for goods and services online or in-store, transferring money to other individuals, and even making bill payments. The rise of mobile payment technologies has led to the development of various payment methods, including mobile wallets, contactless payments, and app-based payment systems.

Types of Mobile Payments

Mobile payments encompass a variety of methods that enable users to make financial transactions using their mobile devices. Here are the primary types of mobile payments:

-

Mobile Wallets: Mobile wallets store users' credit or debit card information securely on their mobile devices. These wallets can be used for both in-store and online purchases. Popular examples include:

-

Apple Pay: Available on iOS devices, Apple Pay allows users to make payments in stores, within apps, and on the web.

-

Google Wallet/Google Pay: Available on Android devices, Google Pay facilitates in-store, online, and in-app purchases.

-

Samsung Pay: Available on Samsung devices, Samsung Pay supports both NFC and Magnetic Secure Transmission (MST) technology, making it compatible with a wider range of payment terminals.

-

Contactless Payments: Contactless payments use Near Field Communication (NFC) technology to enable transactions by simply holding the mobile device close to a payment terminal. This method is quick and secure. Examples include:

-

NFC Payments: Integrated into mobile wallets like Apple Pay and Google Pay, NFC payments are widely accepted at contactless-enabled POS terminals.

-

QR Code Payments: Users scan a QR code displayed by the merchant using their mobile device to complete the payment. This method is popular in regions like Asia, with apps such as Alipay and WeChat Pay leading the way.

-

App-Based Payments: Various apps facilitate mobile payments, often offering additional features like money transfers, bill splitting, and integration with bank accounts. Examples include:

-

PayPal: Allows users to make online purchases, send money to friends and family, and pay for goods and services.

-

Venmo: A social payment app popular in the United States, Venmo enables peer-to-peer payments with a social media twist.

-

Cash App: Developed by Square, Cash App allows users to send and receive money, invest in stocks, and buy Bitcoin.

-

Mobile Banking Apps: Many banks offer their own mobile apps that allow customers to manage their accounts, pay bills, transfer money, and make purchases directly from their bank accounts. These apps provide a comprehensive suite of banking services on the go.

-

Carrier Billing: Carrier billing allows users to charge purchases directly to their mobile phone bill. This method is often used for purchasing digital content like apps, games, music, and other services. The cost is added to the user’s monthly phone bill or deducted from their prepaid balance.

-

Direct Mobile Billing: Similar to carrier billing, direct mobile billing allows users to make purchases that are billed directly to their mobile account. This method is commonly used for microtransactions and is popular in markets with lower credit card penetration.

-

Cryptocurrency Payments: Some mobile payment systems support cryptocurrencies like Bitcoin, Ethereum, and others. These systems use blockchain technology to process payments, offering an alternative to traditional currencies. Examples include:

-

Bitcoin Wallets: Apps like Coinbase, Blockchain Wallet, and Electrum allow users to pay with Bitcoin and other cryptocurrencies.

-

Crypto Payment Gateways: Services like BitPay and CoinGate enable merchants to accept cryptocurrency payments through mobile apps.

-

Proximity Payments: This type of payment involves using Bluetooth Low Energy (BLE) technology to communicate between the mobile device and the payment terminal. While less common than NFC, BLE offers a longer range and can be used in various payment scenarios.

-

Mobile Point of Sale (mPOS): mPOS systems turn mobile devices into portable payment terminals. Businesses can use mPOS apps and hardware to accept card payments anywhere, offering flexibility and mobility. Examples include:

-

Square: Offers a card reader that attaches to a smartphone or tablet, enabling businesses to accept card payments.

-

PayPal Here: Provides a similar service with card readers that work with the PayPal Here app.

Benefits of Mobile Payments

Mobile payments offer numerous advantages that make them increasingly popular for both consumers and businesses. Here are some of the key benefits:

-

Convenience:

-

Ease of Use: Mobile payments eliminate the need to carry physical wallets, cash, or cards. Transactions can be completed with just a smartphone or a wearable device.

-

Anywhere, Anytime: Users can make payments from anywhere, at any time, whether in-store, online, or on the go.

-

Speed:

-

Quick Transactions: Mobile payments are faster than traditional payment methods. Contactless and NFC payments, for example, can be completed in seconds.

-

Reduced Checkout Times: Faster transactions lead to shorter lines and quicker checkouts, enhancing the shopping experience for customers.

-

Security:

-

Advanced Security Features: Mobile payment systems use encryption, tokenization, and biometric authentication (fingerprint or facial recognition) to protect users' financial information.

-

Reduced Fraud Risk: The dynamic nature of mobile payment tokens makes it difficult for hackers to use stolen data for fraudulent transactions.

-

Enhanced User Experience:

-

Integrated Services: Mobile payment apps often include additional features such as transaction tracking, budgeting tools, and loyalty programs.

-

Seamless Integration: Integration with other services like digital wallets, banking apps, and even transit systems makes mobile payments a versatile tool.

-

Cost Efficiency:

-

Reduced Need for Physical Infrastructure: Businesses can save on the costs of handling cash and maintaining traditional payment terminals by using mobile POS systems.

-

Lower Transaction Fees: Some mobile payment services offer lower transaction fees compared to traditional credit card processing fees.

-

Accessibility:

-

Financial Inclusion: Mobile payments can provide financial services to unbanked and underbanked populations, especially in developing countries where smartphone penetration is higher than bank account penetration.

-

Simplified Transfers: Mobile payments make it easy to send and receive money, pay bills, and make purchases without needing a bank account.

-

Increased Customer Engagement:

-

Personalized Offers: Businesses can use mobile payment data to offer personalized promotions and discounts based on customers' purchasing behavior.

-

Loyalty Programs: Many mobile payment apps integrate loyalty programs, allowing customers to earn rewards and incentives for their purchases.

-

Environmental Impact:

-

Reduced Paper Use: Mobile payments reduce the need for paper receipts and billing statements, contributing to environmental sustainability.

-

Less Plastic: With fewer physical cards in circulation, the environmental impact associated with card production and disposal is minimized.

-

Versatility:

-

Multi-Functional: Mobile payment platforms often support multiple currencies and can be used for a variety of transactions, from retail purchases to utility payments.

-

Compatibility: Many mobile payment systems are compatible with various devices and platforms, providing flexibility for both users and merchants.

-

Innovation and Future Potential:

-

Technological Advancements: Mobile payments are at the forefront of technological innovation, incorporating features like blockchain, cryptocurrency transactions, and AI-driven financial insights.

-

Continuous Improvement: The mobile payment industry is constantly evolving, with new features and improvements being introduced regularly to enhance security, convenience, and user experience.

How Mobile Payments Work

Mobile payments facilitate transactions using mobile devices like smartphones and tablets. The process involves several steps to ensure secure, fast, and convenient transactions. Here’s a detailed overview of how mobile payments work:

1. Setup

User Registration and App Installation:

-

Users download a mobile payment app (such as Apple Pay, Google Pay, or Samsung Pay) or use an integrated mobile wallet feature on their device.

-

During setup, users link their bank account, credit card, or debit card to the mobile payment app.

Security Configuration:

-

Users set up security measures such as PIN codes, fingerprint recognition, or facial recognition to authenticate future transactions.

2. Initiation

Selecting the Payment Method:

-

When making a purchase, users open their mobile payment app or activate the mobile wallet by double-clicking a button or tapping the phone screen.

Choosing the Payment Option:

-

Users select the card or account they want to use for the transaction if they have multiple payment methods saved.

3. Authorization

In-Store Payments:

-

NFC Payments: For contactless payments, users hold their device near the NFC-enabled point-of-sale (POS) terminal. The device and terminal communicate wirelessly to initiate the transaction.

-

QR Code Payments: Users scan a QR code displayed by the merchant using their mobile payment app. The app processes the payment using the scanned information.

-

Bluetooth Payments: In some systems, users may pair their device with the merchant’s terminal using Bluetooth Low Energy (BLE) technology.

Online and In-App Payments:

-

When shopping online or within an app, users select the mobile payment option at checkout. They may authenticate the payment using their device's security features.

4. Processing

Encryption and Tokenization:

-

Mobile payment systems use encryption to protect transaction data. The actual card number is not transmitted during the transaction; instead, a token (a unique, encrypted code) is generated and sent to the merchant.

-

This tokenization ensures that the card details remain secure and are not exposed during the transaction.

Transaction Verification:

-

The payment processor or the issuing bank verifies the token and the user's authentication method (PIN, fingerprint, etc.).

-

Upon successful verification, the payment processor approves the transaction.

5. Completion

Confirmation:

-

Once the transaction is authorized, the funds are transferred from the user’s account to the merchant's account.

-

Both the user and the merchant receive a confirmation of the successful transaction.

Receipt Generation:

-

The user receives a digital receipt within the mobile payment app, and the merchant's POS system records the transaction.

Key Technologies Involved

-

Near Field Communication (NFC):

-

NFC is a short-range wireless technology that allows devices to communicate when they are in close proximity. It is commonly used for contactless payments.

-

Tokenization:

-

Tokenization replaces sensitive card information with a unique identifier (token) that can be used to process the payment without exposing actual card details.

-

Biometric Authentication:

-

Biometric authentication methods, such as fingerprint recognition and facial recognition, provide an additional layer of security by ensuring that only the authorized user can initiate a payment.

-

Encryption:

-

Encryption ensures that data transmitted during the payment process is secure and cannot be intercepted or read by unauthorized parties.

Are you looking to develop a mobile payment app like "MyPCS"? Our team at Omninos Solutions specializes in creating secure, user-friendly, and efficient mobile payment applications tailored to your needs.

Why Choose Omninos?

-

Expertise: Extensive experience in mobile app development, especially in the financial and payment sectors.

-

Customization: We tailor our solutions to meet your specific requirements and business goals.

-

Security: Implementation of advanced security measures to protect user data and transactions.

-

User Experience: Focus on creating intuitive and seamless user experiences.

Contact for Live Demo

Website | Contact | Email: info@omninos.com

1. Real-Time Engagement

-

Interactive Experience: A live demo allows potential customers and stakeholders to interact with the app in real-time, providing a hands-on experience that highlights the app's usability and functionality.

-

Immediate Feedback: Engage directly with your audience, gather their reactions, and answer their questions on the spot, allowing for immediate feedback and adjustments.

2. Showcasing Features

-

Comprehensive Overview: Demonstrate all the key features and benefits of your app, from security measures to user interface design, in a structured and detailed manner.

-

Highlight Unique Selling Points: Emphasize what sets your app apart from competitors, such as unique features, superior security, or exceptional user experience.

3. Building Trust and Credibility

-

Transparency: A live demo shows transparency in how your app works, building trust with potential users and stakeholders.

-

Proof of Concept: Demonstrating the app live proves its functionality and effectiveness, reassuring users of its reliability and performance.

4. Enhanced Understanding

-

Visual and Practical Demonstration: Seeing the app in action helps users understand its practical applications and how it can solve their specific problems or improve their processes.

-

Clearer Communication: A live demo can convey complex features and workflows more effectively than written descriptions or static screenshots.

5. Personalized Demonstration

-

Tailored Presentation: Customize the demo to focus on the specific needs and interests of your audience, making it more relevant and impactful.

-

Scenario-Based Use Cases: Present real-world scenarios and use cases that resonate with your audience, demonstrating the app’s practical value.

6. Increased Conversion Rates

-

Engaging Potential Customers: An interactive and engaging demo can significantly increase the likelihood of converting potential customers into actual users.

-

Building Confidence: Demonstrating the app's ease of use and robust features can build confidence and encourage adoption among hesitant users.

7. Competitive Advantage

-

Standing Out: A live demo helps differentiate your app in a competitive market by providing a tangible proof of its capabilities.

-

Innovative Impression: Showcasing your app in a live setting can create an impression of innovation and forward-thinking, appealing to tech-savvy customers.

8. Addressing Concerns Instantly

-

Overcoming Objections: Address any concerns or objections immediately during the demo, reducing barriers to adoption.

-

Clarifying Misconceptions: Clear up any misconceptions about the app's functionality or usability on the spot.

9. Facilitating Decision Making

-

Informed Decisions: Potential customers and stakeholders can make more informed decisions based on a comprehensive understanding of the app’s capabilities and benefits.

-

Visualizing ROI: Demonstrating how the app can improve efficiency, security, and user satisfaction helps stakeholders visualize the return on investment (ROI).

10. Gathering Valuable Insights

-

User Feedback: Collect valuable insights and feedback from participants during the demo, which can inform future improvements and updates.

-

Market Perception: Gauge the market perception and readiness for your app, helping to fine-tune marketing and development strategies.

Share